But two actions on March 23 would swing investors from despair to relief, and reveal who really matters in America.

That morning, the Federal Reserve announced the deployment of additional “tools to support households, businesses, and the U.S. economy overall in this challenging time.” The measures included many actions taken during the 2008 financial crisis, with one new wrinkle: Direct purchases of corporate debt — the first nongovernment bond-buying in the Fed’s history — would now be allowed. Companies have swelled their borrowing in recent years, and experts have identified this as a source of serious economic risk. A sudden shock like the pandemic that wiped out revenues would not only cause bankruptcies, but also accelerate bond defaults, broadening stress throughout the financial system.

Backstopping corporate bond markets would support investors and capital owners. By the evening of March 23, investor confidence was lifted even further; reports announced progress on a record $2.2 trillion congressional rescue package, a large chunk of which would go to support the Fed’s interventions in corporate bond and other markets.

-

The Federal Reserve announced on March 23 that it would start direct purchases of corporate debt — an unprecedented rescue of corporate America.

-

Since then, the stock market has risen over 30 percent, corporate bond funds have recovered, and companies have saved tens of billions in borrowing costs.

-

Thanks to this massive government subsidy, large companies like Boeing and Carnival Cruises were able to avoid taking money directly — and sidestep requirements to keep employees on — by instead issuing bonds.

What would become known as the CARES Act became law on March 27, and the investor class has never looked back. While Americans struggle to file unemployment claims and extract stimulus checks from their banks, while small businesses face extinction amid a meager and under-baked federal grant program, the Fed has, at least temporarily, propped up every equity and credit market in America. And in a testament to its strength, it did so without spending a single cent.

The mere announcement of future spending heartened investors, who have relied on Fed support since the last financial crisis. This explains the shocking dissonance between collapsing economic conditions and the relative comfort on Wall Street. Between March 23 and April 30, the Dow Jones Industrial Average rocketed nearly 6,000 points, a jump of nearly 31 percent, creating over $7 trillion in capital wealth. The April gains were the biggest in one month since 1987.

The same month, 20.5 million Americans lost their jobs.

Similarly, the Fed’s promises to purchase corporate and municipal bonds and asset-backed securities and really anything else uplifted credit markets and made corporate borrowing cheaper, a tangible subsidy for large companies. March ended up setting a record for issuance of investment-grade corporate debt — the safest kind of corporate debt. Two hundred and sixty eight billion dollars traded hands that month, according to a Moody’s Analytics study, and April surpassed it, at $296 billion. Overall, $1 trillion in investment-grade bonds have been issued this year, nearly as much as all of 2019, along with tens of billions more in junk bonds from risky companies, which the Fed has also signaled that it would purchase.

Dozens of companies, from troubled aircraft maker Boeing to airline Delta, from Exxon Mobil to T-Mobile, have been tapping credit markets they might never have been able to access, at lower rates than previously offered. The American Prospect and The Intercept have identified at least 49 large companies that have issued corporate bonds since the Federal Reserve announced that it would purchase them. For some, the benefit of cheaper borrowing was worth hundreds of millions of dollars.

“It is meaningfully changing the way investors are evaluating the risks for a swath of companies,” said Kathryn Judge, a law professor at Columbia University and expert in financial markets and regulations. The Fed’s support disproportionately flows to large corporations with access to credit markets, Joyce pointed out. “Small and midsized businesses with much more need are more likely to struggle.”

-

The Intercept and The American Prospect have identified 49 companies that issued corporate debt since March 23, adding up to hundreds of billions they otherwise couldn’t have secured so cheaply — providing a safety net to the investor class and making a mockery of the alleged virtues of free-market capitalism.

-

This sets the stage for companies with functionally no revenue path in the near future to take on mounds of additional debt – and could set the stage for a series of defaults.

Unlike in 2008, the large corporate entities in line for a bailout didn’t create the crisis in the first place. The Fed’s actions to save corporations from instant bankruptcy, simply by nodding in their direction, beats the alternative. The problem is that this same level of thunderous rescue hasn’t been extended beyond the biggest firms, which could lead to an economic landscape where they dominate society in the very near future. We have a system for central bankers to throw a life preserver to any large corporation, while everyone else must swim several miles to shore themselves.

Congress made the choice to empower the Fed, rather than figure out how to adequately support the rest of the economy and its citizens. And it gave the central bank wide discretion over the process, absolving members of Congress from blame but introducing the Fed’s bias toward large corporations and banks into who gets saved and who doesn’t.

In short, while activists nitpicked about which companies got small business grants worth $10 million, the real bailout, with trillions on the line rather than millions, was happening, quietly, at the Fed.

Investors are supposed to be risk-takers, who earn outsized returns because they put their money on the line. The Fed’s extraordinary support completely flips that, giving a safety net to those who don’t need it and making a mockery of the alleged virtues of free-market capitalism. If nothing the wealthy ventures can be lost, the only people who bear risks in our society are those who don’t have any money to begin with. That’s a recipe for soaring sales in pitchforks.

But what the Fed is doing may not even be sufficient to protect capital. The week of May 11 saw the biggest percentage drop in the stock market in nearly two months. As the Fed actually starts to actually outlay money, even it recognizes that not every crisis can necessarily be solved by lending gobs of money to General Electric. Not only is it socially unsustainable to protect just the rich from a crisis of this magnitude, it may not even work.

Among other measures, the CARES Act appropriated $454 billion to the Treasury Department’s Exchange Stabilization Fund to be used as an equity stake in a series of Fed “credit facilities.” You can think of this as similar to a big bank. The ESF stake represents the deposit base, which can absorb any losses from Fed lending. (In reality, the Fed is perfectly able to take losses through various accounting gimmicks, but it has chosen to limit itself in this fashion.) The Fed can then lever those deposits up 10 to 1, the same way a bank loans well above its deposits. That created a $4.5 trillion — trillion with a T — money cannon to back up the promises.

As soon as it became clear that a $4.5 trillion slush fund would be created, equity markets ballooned. The total value of the stock market cratered to 103 percent of GDP, about $21.8 trillion, on March 23. By April 30 it was back to 136.3 percent of GDP, or $28.9 trillion. By that metric, $7.1 trillion in stock market wealth has been created in that period.

Not only is it socially unsustainable to protect just the rich from a crisis of this magnitude, it may not even work.

It’s not like there were any other positive stories in the economy in late March and April, so we can attribute most of this uplift to the establishment of Fed facilities. “The Fed is the action, it’s the only real action,” Marcus Stanley, policy director with the coalition Americans for Financial Reform, told me. Almost all of that benefit goes to the wealthy: A 2017 report showed that about 10 percent of Americans own 84 percent of all stocks.

More critical was the rescue of the credit markets. By March 23, investors had spent a few weeks engaged in fire sales of corporate debt. Cash was fleeing to the safety of Treasury bonds. Reluctance to take on corporate debt triggered higher borrowing costs everywhere, and while bond-buying was still going on, many companies found themselves stuck. “There was like 10 or 15 days, there was no bond issue,” said V. Prem Watsa, CEO of Fairfax Financial Holdings, in a May 1 earnings call. “No one could do a bond issue. The AAA company couldn’t do a bond issue.”

The Fed’s announcement changed the picture. “It’s signaling, ‘We will not let the bond market go low,’” Stanley said. “’We’ll put a floor under the bond market in an aggressive and historically unprecedented way.’”

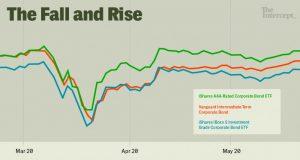

You can best see this through an array of exchange-traded funds, or ETFs: investment funds traded on stock exchanges made up of securities in a particular economic sector or asset class. There are dozens of ETFs linked to corporate debt, and their charts around this period all resemble a panoramic view of the Grand Canyon, hitting a low point on March 23, before shooting back up.

On March 23, the BlackRock iShares ETF of investment-grade corporate bonds went up 7.39 percent. The iShares AAA-rated corporate bond ETF: up 7.52 percent. Vanguard’s intermediate-term corporate bond ETF: up 5.43 percent. Pimco’s investment-grade corporate bond ETF: up 7.06 percent.

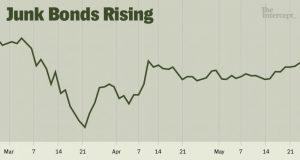

Even “high-yield” corporate bond ETFs, which hold debt in riskier companies imperiled by the crisis, have this same shape. The effect is often delayed until April 9, when the Fed announced that it would actually buy high-yield ETFs, in an indirect bid to reach so-called junk bonds that highly leveraged and risky corporations issue to investors. The iShares iBoxx high-yield ETF saw its biggest move upward that day since 2008. Other high-yield ETFs like Deutsche X-trackers and the S&P high-yield bond index show a similar spike. Junk bond issuance similarly spiked.

The Fed announcements included intentions to buy municipal bonds, as well as securities backed by student loans, auto loans, credit card debt, and commercial real estate loans; to make direct loans to large and midsized businesses; and to guarantee the entire trillion-dollar money market fund industry. It sent the message that essentially every credit market in existence would get some form of assistance. “They consider themselves a lender of last resort,” Peter Boockvar of Bleakley Advisory Group told CNBC. “They’re now the lender of all resorts.”

But the corporate bond rescue was particularly useful to companies sinking under the weight of the economic crash.

Carnival Cruise Lines is nobody’s idea of a sustainable business at the moment. Reeling from a Covid-19 outbreak on its Diamond Princess ship and shut down thereafter, in mid-March, Carnival was flirting with a consortium of hedge funds on a high-interest loan above 15 percent. These vulture funds, including Apollo Global Management and Elliott Management, specialize in distressed debt, squeezing governments and businesses with no alternatives. If Carnival couldn’t repay the loan, the hedge funds would be primed to take ownership.

But the March 23 announcement, signaling a Fed backstop to all comers, suddenly gave Carnival new options. Within days, it had secured $5.75 billion in loans, including a $4 billion bond issuance at 11.5 percent interest, and a $1.75 billion bond at an even smaller 5.75 percent rate that could be converted into Carnival stock. Because we know the alternative was a loan with 15 percent interest, we can calculate the value to Carnival. The difference in interest on the $4 billion loan is at least $140 million, and on the overall package, closer to $310 million.

Carnival also sold equity stakes of $500 million after March 23 (including 8 percent of the company to Saudi Arabia’s sovereign wealth fund), less than the $1.25 billion the vulture funds were seeking. That’s an implicit subsidy of $750 million. Keeping more of the company in shareholders’ hands gives them a subsidy as well. In addition, Carnival’s market capitalization grew by $3.5 billion from March 23 to the end of April. So one company with essentially no social or economic function currently benefited from billions in Fed-induced support.

Another good example is Boeing, the basket-case aircraft maker with a sketchy record of keeping planes in the sky. The firm “rejected” a federal bailout after issuing $25 billion in bonds. But that bond issuance was entirely made possible by the Fed’s implicit guarantee of corporate bond markets. Boeing’s Chief Financial Officer Greg Smith admitted on March 24, a day after the Fed announcement, that credit markets were “essentially closed.” A month later, it made the sixth-largest bond issuance in U.S. history that left investors clamoring for more; over 600 investors were willing to take up to $70 billion in Boeing debt at the auction.

So Boeing didn’t avoid a bailout; it got one through the side door from the Fed. And the company knows it: Smith thanked the Trump administration after securing the loan, “for the actions they have taken to support our economy and the credit markets.”

Boeing’s bond rescue had a secondary benefit. The CARES Act set aside $17 billion in a Treasury-led bailout for firms “critical to national security,” which everyone recognized as code for Boeing. That money would have come with significant strings attached, like equity stakes for the government. By the Fed reopening credit markets to Boeing, the company sidestepped that condition and kept its investors whole. “Without the Fed action, Boeing would be significantly owned by the U.S. taxpayer,” said Dennis Kelleher of the Wall Street watchdog Better Markets. That’s an implicit subsidy to Boeing and its shareholders.

The lack of conditions had a human cost. Aviation-related grants that the Treasury supplied came with a requirement to keep workers on the payroll for six months. Freed from any restrictions, Boeing almost immediately announced that it would cut 16,000 jobs. Similarly, General Electric, another company that spurned a direct bailout and floated $6 billion in bonds, cut 13,000 jobs in its aviation unit shortly thereafter.

Within weeks of the March 23 announcement, many large companies had wandered over to the corporate bond trough and taken a sip. Issuance of corporate bonds in April alone jumped to three times as much as the year before. The three largest weeks in the history of corporate debt offerings were two weeks in April and the first week of May.

Exxon Mobil took $9.5 billion. Nike was good for $6 billion, with $5 billion for Procter & Gamble and $6.5 billion for McDonald’s. Apple grabbed $8.5 billion. There was $11 billion for Disney and $6.5 billion for Coca-Cola. Silicon Valley stalwart Oracle trumped them all with a $20 billion debt offering. And Fairfax Financial Holdings, whose CEO, Watsa, was complaining that nobody could get a bond, secured $650 million at the end of April. “The bond market opened up,” Watsa told analysts on the earnings call. “Federal Reserve has been fantastic. The CARES Act has been huge.”

Bond recipients included companies battered by the coronavirus crisis. “April’s worst month for U.S. business activity in perhaps more than 85 years did not prevent high-yield bond issuance from topping its year earlier pace by 19 percent,” Moody’s noted. That included an $8 billion high-yield bond for Ford, the largest speculative bond sale in history.

“They consider themselves a lender of last resort. They’re now the lender of all resorts.”

Delta Airlines managed a $5 billion bond issue, despite few flights in the air; Southwest raised $6 billion. Norwegian Cruise Lines, in the same boat as Carnival, secured $2.2 billion. Six Flags Entertainment, shuttered due to lockdowns, got $725 million. MGM Resorts, a luxury series of hotels and casinos, took in $500 million. No AMC movie theater was open, but AMC floated $500 million in debt anyway. Despite housing few travelers, Airbnb took $1 billion.

Investors deemed just one major company too risky for bonds: United Airlines, which begged off a $2.25 billion bond deal on May 12 because investors wanted more protections attached to the loan and a higher interest rate than United sought. But despite the fact that banks and investors are in position to demand better terms, interest rates are correspondingly lower than what these companies would have been forced to agree to before the Fed’s intervention.

It was also significantly cheaper for companies to borrow money at the beginning of May than it was in late March. The corporate bond spread (the difference in interest-rate yield between the corporate bond and Treasury bonds) for BBB-rated firms, just above investment grade, soared throughout February and March and peaked on, you guessed it, March 23, at 4.88 percent. By May 1, it was down to 2.83 percent. The high-yield corporate bond spread looks the same, peaking at 10.87 percent on March 23 and settling at 7.7 percent on May 1. Those spreads have continued to drop. A lower spread equates to tangibly lower borrowing costs for large firms.

In all, The American Prospect and The Intercept found published reports of bond sales for 49 companies, a total of at least $190.3 billion. Some bond amounts were undisclosed, like for General Mills, CVS, and Kroger, so the number is likely higher. The interest savings on those bond issuances due to Fed intervention is hard to calculate, but using Credit Flow Research’s post-announcement bond issuance estimate of $575 billion, and the changes in spreads after March 23, it’s clearly tens of billions of dollars.

And, given that one part of the credit hierarchy gives the rest a boost, the market uplift to investors in the $10 trillion corporate debt market would be calculated in the hundreds of billions. Combined with ETF and stock market uplift, the trillions in relief absolutely dwarfs what regular Americans got to tide them over during the crisis.

This unprecedented rescue of corporate America, done without the outlay of a single U.S. dollar, was described by Fed Chair Jerome Powell in an April 29 news conference as not only necessary, but positive. “Many companies that would’ve had to come to the Fed have now been able to finance themselves privately … and that’s a good thing,” Powell explained. It is somewhat positive that distressed companies could turn to regular credit markets instead of bottom feeders like private equity vultures or Warren Buffett. And because of the existing connections to flood the financial system with money, bailouts are almost literally as simple as turning on a light switch.

Congress didn’t have to cede authority to the Fed and carp about it after the fact.

But to properly assess the virtues of the rescue, you have to set it in context. The unemployment rate is 14.7 percent and rising. Car lines for food banks stretch for miles. As Americans continue to struggle and lose ground, the nation’s investment elite have been thus far saved from any downside of the coronavirus crisis. Beneficiaries are largely confined to stockholders, bondholders, and corporate executives (who are often major stockholders). Workers are not only not protected, they’re paying for the rescue, with taxpayer money propping up the Fed actions.

“This is a massive wealth transfer to owners of financial assets,” said Lev Menand, a former Treasury official who now teaches at Columbia University. “The rules of the game are supposed to be that equities take the loss, high-yield debt holders take the loss.” Allowing them to instead bear no burden is a form of socialism for capitalists.

It would perhaps be more tolerable if anyone other than the rich shared in the gains of this corporate rescue. But the Fed’s bond-buying program, unlike the Paycheck Protection Program, has no requirements on companies to retain workers. The Fed changed the term sheets between March 23 and April 9, eliminating any such requirements. Apple’s recent debt issuance, which could later be purchased directly or indirectly by the Fed, explicitly states that it will be used for, among other things, “share buybacks and dividends” — forms of leaking money to investors rather than keeping workers on payroll.

In addition, the Fed has essentially outsourced its bond-buying and loan-making authority to big money managers and banks, heightening the need for connections with these giants to get relief. Smaller companies, who don’t have the revenue or technical know-how to issue bonds into public markets, will find it more difficult to get in line for relief. Meanwhile, lending to small businesses and individuals has slowed as banks pull back during the crisis; by one count, interest rates charged to small businesses are now double the rates for large firms. Running bailouts through the Fed necessarily enhances the survival of large financial players and big corporations; everyone else must fight for crumbs.

Treasury Secretary Steven Mnuchin responded to this charge of special benefits for large corporations at a Senate Banking Committee hearing on May 19, essentially calling the stealth bailout a good thing. “The announcement of the corporate bond facility without putting up $1 of taxpayer money unlocked the entire primary and secondary market for corporate bonds,” Mnuchin said. “Companies that I had expected would need to borrow from us were able to borrow $25 billion in the primary markets” — a reference to Boeing.

Congress didn’t have to cede authority to the Fed and carp about it after the fact. It could have decided the parameters of any economic rescue. But that would involve making actual governing decisions, which Congress would rather defer to others. You can argue that, in the absence of state functionality, the Fed had to step in. But we’re living with the unequal consequences of a central bank that can only solve problems for one set of powerful interests. And perversely, rescuing investors — rich people like members of Congress and the donors they listen to — makes it easier for Congress to keep ignoring the needs of everyone else.

Even the Fed understands this at some level. On May 13, Powell pleaded with Congress to pass stronger fiscal aid to prevent a multiyear economic malaise. “Deeper and longer recessions can leave behind lasting damage to the productive capacity of the economy,” he said.

On May 12, the Fed finally kicked off its corporate bond-buying program, 50 days after the fateful March 23 announcement. It was confined to purchasing corporate bond ETFs of once investment-grade “fallen angel” companies that had gone to junk. Within two days, $305 billion had been purchased. But while the purchases sent corporate bonds up in value, by and large the promise of bond-buying had already produced the desired effect. The Fed completed the bailout before ever administering it.

“This is more like August 2007 than September 2009.”

Some market watchers see the runaway rally in capital markets as irrational. “People that manage large portfolios and assets spent 10 years in a bull market fed by Federal Reserve intervention,” said Menand. “Their frame of reference is that something goes wrong and the Fed comes in, that’s a market opportunity.” Menand believes that the Fed won’t be able to sustain such valuations amid mass bankruptcies and high unemployment.

With the hope of a V-shaped economic recovery now completely dead, at some point the markets will have to take notice, and the sugar high from the Fed aiming its money cannon will wear off. Stocks fell modestly in May, and Goldman Sachs analysts have predicted a 20 percent drop in the next three months. Noted hedge fund manager David Tepper called the stock market in the first half of May the second-most overvalued market in his career, rivaled only by the dot-com boom. And in raw numbers, the valuation increase has gone well beyond the amounts the Fed has promised.

That’s what you get when you send the Fed in to handle a problem in the real economy. The Fed is ill-suited as a crisis manager; it sees its job as mainly to boost liquidity and keep assets strong.

“You can get loans, but loans don’t replace income,” said Nathan Tankus, research director at the Modern Money Network. Menand likened the moment to August 2007, when the Fed provided enough liquidity to avert crisis for a while. Eventually, there was a reckoning when asset prices declined and losses hit the system. “This is more like August 2007 than September 2009,” he said. “The idea that we won’t have massive insolvency at big companies is crazy. And the Fed will not be there.”

The Fed-induced rush into corporate bonds, in other words, pools risk in an unstable asset, creating the type of financial crisis it seeks to stamp out. Companies with functionally no revenue path in the near future taking on mounds of additional debt could set the stage for a series of defaults, which rose in April. Zombie companies being kept alive by debt markets eventually run up against the fundamentals of operating amid an economic depression. And indebted companies stave off liquidation by firing workers, as Hertz did last month to avoid bankruptcy. It didn’t help; Hertz filed for Chapter 11 on May 22.

The very knowledge that the Fed will save investors from trouble is likely to accelerate risk throughout the market. “If you told a family you can get a credit card at 18 percent [interest], but in a downturn we will give you an opportunity to get a 3 percent card, that would incentivize them to spend a lot of money,” Bharat Ramamurti, one of the members of the Congressional Oversight Commission, told me.

The Fed itself has called out this possibility. Powell’s comments on May 13 were accompanied by a May 15 financial stability report, warning that the financial system had “amplified the shock” of the coronavirus crisis. It raised concerns about debt defaults as its actions persuaded investors to buy up more debt. It warned that asset prices had “room to fall,” when the announcement effect created more of that room. It worried of defaults among high-risk “leveraged loans,” when these are precisely the kind of loans it’s vowed to buy through purchases of high-yield ETFs.

Just how deeply does the Fed have its fingers in the dough of the economy? Recent job growth numbers reflect what you’d guess — that the most rapid job creation is happening at general merchandise stores like Walmart and Costco. Right behind them are “monetary authorities-central banks.”

First published on The Intercept.

Shared via Creative Commons.